Key outlook takeaways

- Significantly harsher than expected tariffs from the new US administration have derailed a 2.5 year bull market for European equities as investors price in the chances of a recession.

- Despite the pause in “reciprocal” tariffs, we expect elevated volatility to continue, as uncertainties remain high, and the remaining tariffs will have implications for corporates and the broader economy.

- We recommend maintaining a defensive bias and caution regarding sectors that are likely to suffer from persistently high tariffs.

- Our core principles remain as important as ever: long-term thinking, a focus on companies’ intrinsic value, and the proper management of portfolio risks.

Market nose-dive

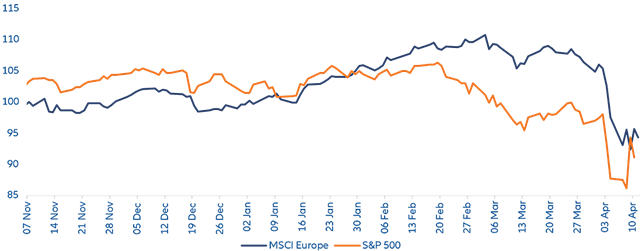

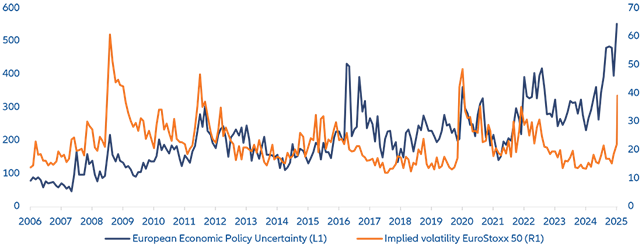

President Trump’s harsh implementation of his ideas on tariffs has derailed the European equity market, which had not experienced a double-digit setback for around 2.5 years – MSCI Europe saw a total return of 55% since Sep 2022, before the latest correction. With a 17%decline since this year’s high in early March, followed by a 5% rebound driven by President Trump’s U-turn on tariffs on 9 April, MSCI Europe and the S&P 500 have both lost more than their gains since the US election. Initial enthusiasm for business-friendly political measures gave way to increasing uncertainty and concerns about the impact on growth and inflation of measures such as tariffs, the dismissal of civil servants, and the mass deportation of illegal immigrants.While European corporate earnings have so far held at decent levels (see chart below), the market has started to price in increased recession probabilities for the US and Europe under scenarios where significant US tariffs and retaliatory tariffs are being maintained, coupled with potentially meaningfully higher inflation in the US. Off a relatively reasonable valuation level compared to the US at the beginning of March of 14.8x 12 month forward earnings, European equities have derated to 12.6x, slightly below their 20-year average of 13.0x. Similar to its US counterpart VIX, implied volatility for the Euro Stoxx 50 spiked from 21 to 53 (currently ~34) during the week of the US tariff announcement on April 2. Technical indicators like the relative strength index (RSI) are now clearly in oversold territory for Europe and the US, while typical investor sentiment indicators like the AAII US Investor Survey are also at bearish levels. These indicators point to very negative sentiment and may be considered an entry point for investors who follow the philosophy of Warren Buffet: “Be fearful when others are greedy and greedy when others are fearful.”Chart 1: MSCI Europe and S&P 500 performance since US presidential election (indexed to 100, local currencies)

Source: Bloomberg as of 11 April 2025. Past performance is not indicative of future performanceChart 2: Economic uncertainty index and implied volatility – Euro Stoxx 50

Source: Bloomberg as of 11 April 2025. Past performance is not indicative of future performanceChart 2: Economic uncertainty index and implied volatility – Euro Stoxx 50 Source: Bloomberg as of 11 April 2025

Source: Bloomberg as of 11 April 2025Have we reached the bottom?

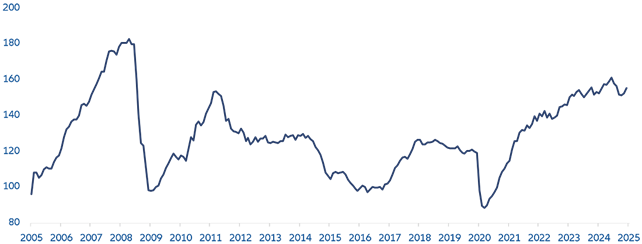

While one might read from the above-mentioned indicators that the market might not be far from the bottom, for now this is only likely for the very short term. Whether markets will see a V-shaped recovery or take a further hit depends on developments on the tariff front and whether or nor a recession will eventually ensue (see below for more on tariffs). Current consensus earnings forecasts, which stand at 6% EPS growth for MSCI Europe in 2025 (cf.: S&P 500: +11%), will almost certainly have to come down.The upcoming 1Q25 reporting season will be watched eagerly to get further direction, but with visibility for companies probably as limited as for anybody else right now, any guidance is unlikely to be very meaningful or particularly positive. We thus believe it is unlikely that the reporting season will be a positive catalyst. While definitely not our base, we note that in a typical recession, earnings forecasts are revised down by 20%-30% from peak-to-trough, hence the current market valuation at ~3% below long-term average does not yet incorporate a recession.Chart 3: MSCI Europe 12m forward consensus EPS

Unprecedented tariff situation

Despite President Trump’s U-turn, the effects from tariffs continue to concern, on top of which comes the fact that the situation remains completely unpredictable. Even under this new scenario, the weighted average tariff into the US will still increase significantly from 2.5% to 18%, given the prevailing 10% universal tariff and 145% on China. Also, tariffs on autos are still in place, and tariffs on pharma have yet to come.While many observers and investors initially assumed that Trump would use the tariffs as a negotiating tactic, this view has increasingly given way to the realization that this is not the case and that more fundamental economic and political goals are being pursued. This makes simply “negotiating away” with “deals” between trade partners a less likely outcome. The extent of the long-term implications for the global economic system can hardly be estimated as yet, but on balance they are certainly negative for the global economy and therefore represent a potential longer-term negative factor for equities.On a more positive note, the change in course means the Trump administration is not as resistant to market pain as it seemed for a while. The strong decline in US equities and a spike in US treasury yields apparently couldn’t be ignored any longer. The planned announcement of tax cuts – if approved by Congress – could provide a positive stimulus in the coming weeks, though mounting concerns about US debt sustainability suggest overly generous tax cuts could also be taken negatively by the market.How to invest?

We believe that equity market volatility is likely to remain elevated in the coming months. Significant growth-inhibiting tariffs remain in place, and are not yet reflected in consensus earnings forecasts, “deals” with trading partners have yet to be concluded, and uncertainty on the corporate side is likely to persist for the time being, leading to temporarily lower investments in view of the erratic decisions taken by the US administration to date. In periods of such elevated uncertainty, we recommend positioning portfolios with a defensive and quality bias and an underweight in clear losers from first and second order effects from tariffs (e.g. automotive or apparel & footwear). Corporates are impacted by the same uncertainty as investors. Without a reliable and predictable framework, there is limited appetite to invest or re-allocate production. This uncertainty will have a negative impact for growth and the earnings outlook. In these times, it is also good to go back to the basic principles of investing: managing portfolio risks properly, thinking long-term, and focusing on the intrinsic value of companies.Despite risks from tariffs, we favour European over US equities. Europe’s growth gap to the US is likely to narrow, higher public investment spending in Europe will support growth, lower inflation risks in the Eurozone allow the ECB to ease more quickly than the Fed, and Europe’s valuation discount to the US remains well below the long-term.Want to search and invest in related funds?Open the WeLab Bank App and click【Featured Funds】to find out more!Importance NoticeThis document is for general information only. The information or opinion herein is not to be construed as professional investment advice or any offer, solicitation, recommendation, comment or any guarantee to the purchase or sale of any investment products or services. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. The investment products or services mentioned in this webpage are not equivalent to, nor should it be treated as a substitute for, time deposit, and are not protected by the Deposit Protection Scheme in Hong Kong.The information or opinion presented has been developed internally and/or taken from sources (including but not limited to information providers and fund houses) believed to be reliable by WeLab Bank, but WeLab Bank makes no warranties or representation as to the accuracy, correctness, reliabilities or otherwise with respect to such information or opinion, and assume no responsibility for any omissions or errors in the content of this document. WeLab Bank does not take responsibility for nor does WeLab Bank endorse such information or opinion.Investment involves risks. The price of an investment fund unit may go up as well as down and the investment funds may become valueless. Past performance is not indicative of future results. WeLab Bank makes no representation or warranty regarding future performance. Any forecast contained herein as to likely future movements in interest rates, foreign exchange rates or market prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in interest rates, foreign exchange rates or market prices or actual future events or occurrences (as the case may be).You should not make any investment decision purely based on this document. Before making any investment decisions, you should consider your own financial situation, investment objectives and experiences, risk acceptance and ability to understand the nature and risks of the relevant product(s). WeLab Bank accepts no liability for any direct, special, indirect, consequential, incidental damages or other loss or damages of any kind arising from any use of or reliance on the information or opinion herein. You should seek advice from independent financial adviser if needed.WeLab Bank is an authorised institution under Part IV of the Banking Ordinance and a registered institution under the Securities and Futures Ordinance (CE Number: BOJ558) to conduct Type 1 (dealing in securities) and Type 4 (advising on securities) regulated activities.This document is issued by WeLab Bank. The contents of this document have not been reviewed by the Securities and Futures Commission in Hong Kong.