- The healthcare sector exhibited superior performance compared to the overall market in 2022 and has continued to generate positive returns during the first half of 2023. This is consistent with its track record of minimizing losses during significant market downturns.

- Simultaneously, there has been a surge in global demand for healthcare services and advancements in medical technology, which has contributed to revenue growth in various segments of the sector.

- The combination of defensive characteristics and growth opportunities could be a valuable source of diversified returns.

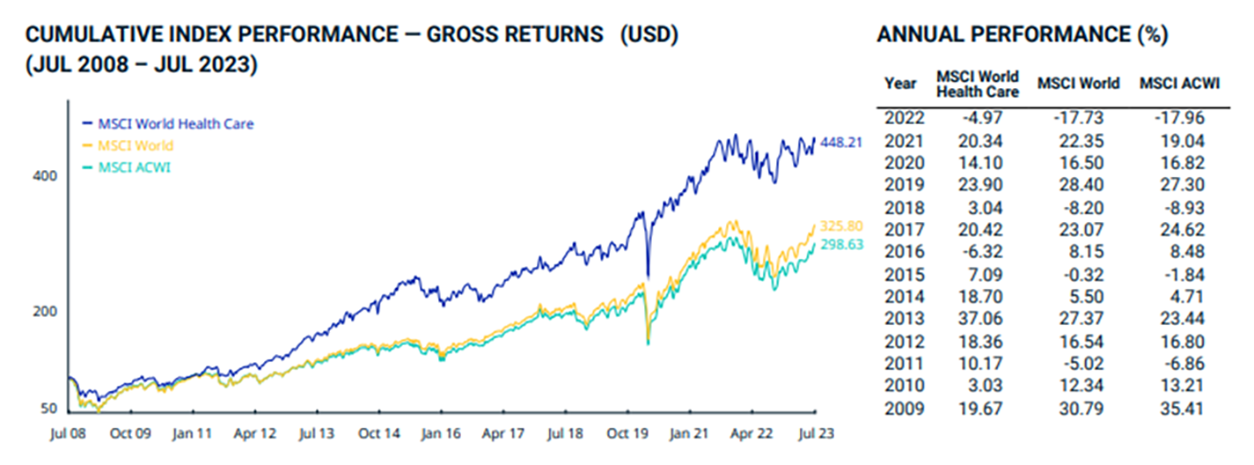

The healthcare sector continues to witness a steady and escalating global demand for medical care services, which has been instrumental in upholding its resilience during market downturns. This was clearly evident in 2022, as exemplified by the MSCI World Health Care Index's return of -5.4%, compared with MSCI World Index's decline of -17.7%. Moreover, during the period from January to July 2023, the MSCI World Index has already recorded a substantial increase of 19.34%, while the MSCI World Health Care Index exhibited a mild growth of 2.43%. Nevertheless, it is important to note that the healthcare sector is also experiencing notable expansion, presenting investors with an additional potential avenue for diversified returns.

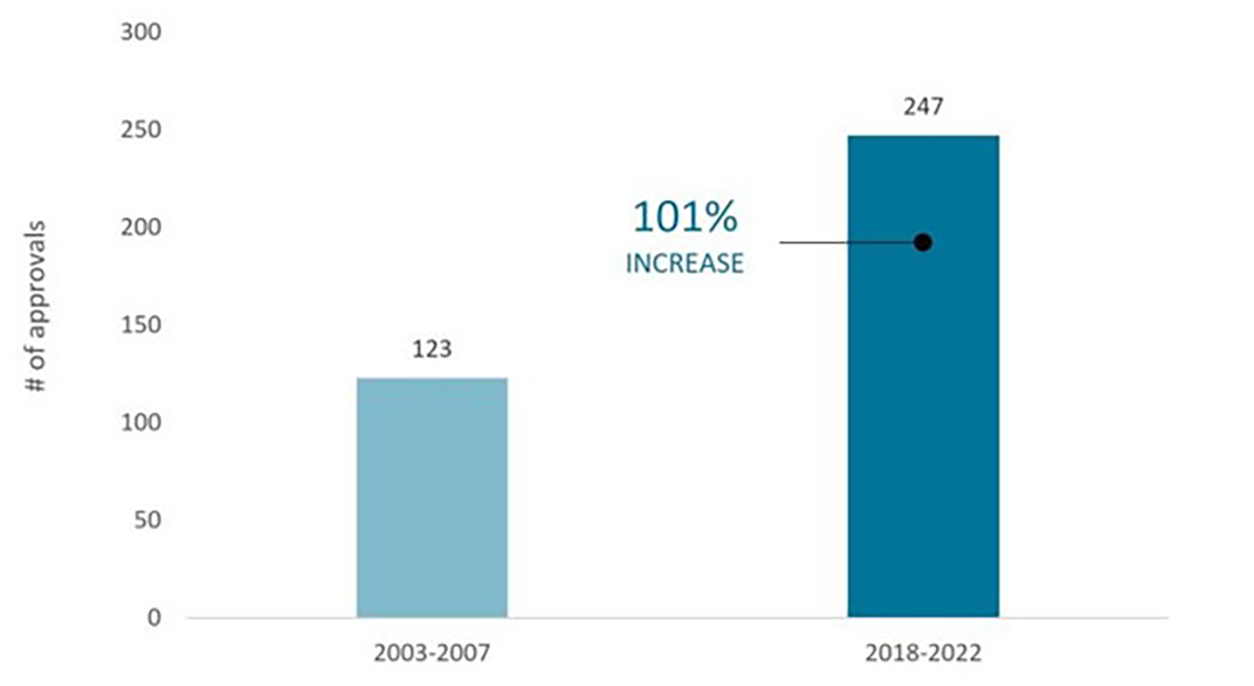

The healthcare sector continues to witness a steady and escalating global demand for medical care services, which has been instrumental in upholding its resilience during market downturns. This was clearly evident in 2022, as exemplified by the MSCI World Health Care Index's return of -5.4%, compared with MSCI World Index's decline of -17.7%. Moreover, during the period from January to July 2023, the MSCI World Index has already recorded a substantial increase of 19.34%, while the MSCI World Health Care Index exhibited a mild growth of 2.43%. Nevertheless, it is important to note that the healthcare sector is also experiencing notable expansion, presenting investors with an additional potential avenue for diversified returns. Rapid innovation and growthThe advancements in genomic sequencing and other biomedical tools over the past two decades have revolutionized the field of disease targeting and treatment. These breakthroughs encompass a wide range of methods, including antibody drug conjugates, gene therapies, and remote glucose monitors, which have the potential to significantly enhance the standard of patient care. In some cases, rare diseases that were once considered incurable can be addressed.In order to foster and support such research endeavors, regulatory authorities have established expedited pathways for the review process of medications that target high unmet medical needs. As a result of these initiatives, there has been a remarkable increase in the number of newly approved drugs. Specifically, from 2018 to 2022, the Food and Drug Administration (FDA) granted approval to nearly 250 novel drugs, representing a 100% surge compared to the approvals granted 15 years ago (Image 1). Similarly, during the same five-year period, the European Medicines Agency (EMA) approved over 200 therapies.Image 1: Food and Drug Administration (FDA) approvals of novel drug

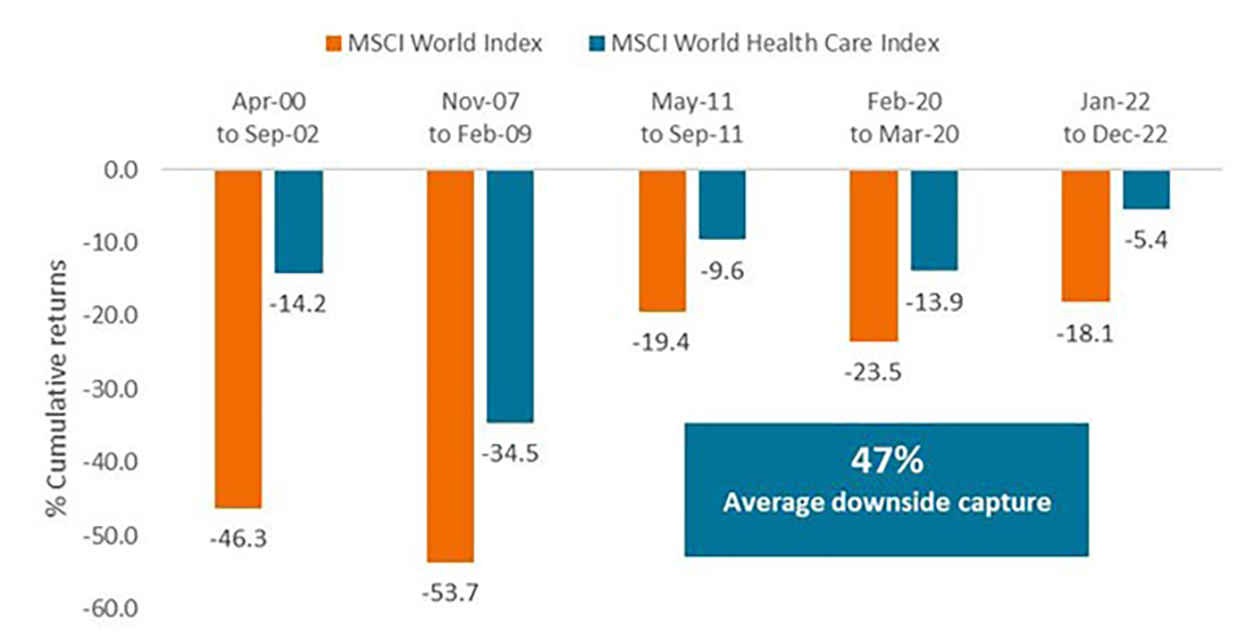

Rapid innovation and growthThe advancements in genomic sequencing and other biomedical tools over the past two decades have revolutionized the field of disease targeting and treatment. These breakthroughs encompass a wide range of methods, including antibody drug conjugates, gene therapies, and remote glucose monitors, which have the potential to significantly enhance the standard of patient care. In some cases, rare diseases that were once considered incurable can be addressed.In order to foster and support such research endeavors, regulatory authorities have established expedited pathways for the review process of medications that target high unmet medical needs. As a result of these initiatives, there has been a remarkable increase in the number of newly approved drugs. Specifically, from 2018 to 2022, the Food and Drug Administration (FDA) granted approval to nearly 250 novel drugs, representing a 100% surge compared to the approvals granted 15 years ago (Image 1). Similarly, during the same five-year period, the European Medicines Agency (EMA) approved over 200 therapies.Image 1: Food and Drug Administration (FDA) approvals of novel drug The emergence of new therapies coincides with a significant surge in the demand for medical care. This increased demand can be attributed to factors such as the growing household wealth and the expansion of both public and private insurance coverage. For instance, in China, government reforms implemented over the past decade have resulted in approximately 95% of the population being covered by the country's basic insurance program. Moreover, China's reimbursement for pharmaceuticals has also expanded, with more than 100 therapies being added to the National Reimbursement Drug List in 2022.Another influential factor contributing to the rising demand for medical care is the aging global population. It is projected that by 2050, approximately 16% of the world's population will be over the age of 65. This demographic group tends to spend around three times more on healthcare compared to younger individuals. This demographic shift is particularly significant in high-income regions.The combination of rapid innovation and increased demand has led to substantial revenue growth in the healthcare sector. Sales of blockbuster biotech drugs, which are defined as drugs with annual sales of $1 billion or more, surpassed $400 billion in 2021, marking a seventy-fold increase compared to approximately two decades ago. Furthermore, the market for COVID-19 products, which did not exist three years ago, contributed $75 billion to the total revenue in the same year.The Defense Proof PointsIn the face of increasing interest rates impacting financial markets, the healthcare sector exhibited superior performance compared to broader equity indices. This trend is not an isolated occurrence. Over the period from 2000 onwards, healthcare has consistently demonstrated resilience by experiencing only a 47% average exposure to market downturns of 15% or more (refer to Image 2). This can be attributed, in large part, to the strong performance of large-cap health insurance and pharmaceutical companies. These entities, characterized by stable demand and pricing power, have shown a capacity to thrive irrespective of the prevailing economic conditions.Image 2: Healthcare has outperformed in past drawdowns

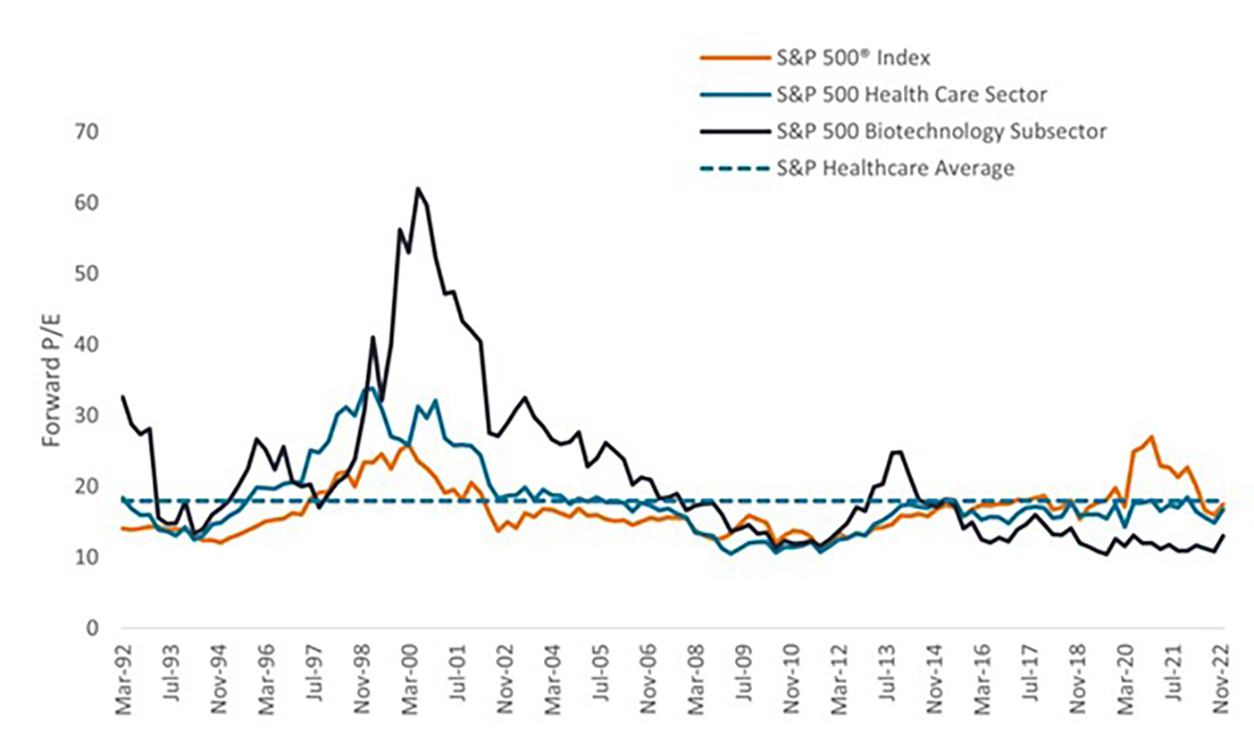

The emergence of new therapies coincides with a significant surge in the demand for medical care. This increased demand can be attributed to factors such as the growing household wealth and the expansion of both public and private insurance coverage. For instance, in China, government reforms implemented over the past decade have resulted in approximately 95% of the population being covered by the country's basic insurance program. Moreover, China's reimbursement for pharmaceuticals has also expanded, with more than 100 therapies being added to the National Reimbursement Drug List in 2022.Another influential factor contributing to the rising demand for medical care is the aging global population. It is projected that by 2050, approximately 16% of the world's population will be over the age of 65. This demographic group tends to spend around three times more on healthcare compared to younger individuals. This demographic shift is particularly significant in high-income regions.The combination of rapid innovation and increased demand has led to substantial revenue growth in the healthcare sector. Sales of blockbuster biotech drugs, which are defined as drugs with annual sales of $1 billion or more, surpassed $400 billion in 2021, marking a seventy-fold increase compared to approximately two decades ago. Furthermore, the market for COVID-19 products, which did not exist three years ago, contributed $75 billion to the total revenue in the same year.The Defense Proof PointsIn the face of increasing interest rates impacting financial markets, the healthcare sector exhibited superior performance compared to broader equity indices. This trend is not an isolated occurrence. Over the period from 2000 onwards, healthcare has consistently demonstrated resilience by experiencing only a 47% average exposure to market downturns of 15% or more (refer to Image 2). This can be attributed, in large part, to the strong performance of large-cap health insurance and pharmaceutical companies. These entities, characterized by stable demand and pricing power, have shown a capacity to thrive irrespective of the prevailing economic conditions.Image 2: Healthcare has outperformed in past drawdowns Attractive ValuationsIn recent months, investors have displayed a greater inclination to reward innovation, resulting in notable gains (100% or more) for certain stocks upon the release of positive news. These favorable returns are facilitated by attractive valuations in the healthcare sector. The forward price-to-earnings (P/E) ratio of the sector currently resides below its long-term average (refer to Image 3), and numerous biotech companies are trading at prices lower than the value of cash on their balance sheets. The alluring low valuations have also piqued the interest of large-cap biopharma companies, as evidenced by several mergers and acquisitions announced last year at premiums exceeding 100%. Given the impending patent cliffs faced by certain biopharma companies in the coming decade, anticipate the possibility of further deals materializing in 2023.Image 3: The valuations of healthcare have fallen to below average levels

Attractive ValuationsIn recent months, investors have displayed a greater inclination to reward innovation, resulting in notable gains (100% or more) for certain stocks upon the release of positive news. These favorable returns are facilitated by attractive valuations in the healthcare sector. The forward price-to-earnings (P/E) ratio of the sector currently resides below its long-term average (refer to Image 3), and numerous biotech companies are trading at prices lower than the value of cash on their balance sheets. The alluring low valuations have also piqued the interest of large-cap biopharma companies, as evidenced by several mergers and acquisitions announced last year at premiums exceeding 100%. Given the impending patent cliffs faced by certain biopharma companies in the coming decade, anticipate the possibility of further deals materializing in 2023.Image 3: The valuations of healthcare have fallen to below average levels While the healthcare sector faces various challenges such as labor shortages, regulatory pressures, and declining sales related to COVID-19 would continue to bring negative effect on certain stock names. However, the long-term outlook of the healthcare sector more than makes up for any near-term headwinds. The opportunity to generate returns that are not closely corrected – while simultaneously delivering benefits for patients – is becoming increasingly robust.Our Featured Funds Services consolidate investment ideas and hot funds1. “Healthcare” is one of the themes available in the Services. Log in to WeLab Bank app, tap the “GoWealth” at the right bottom corner > “Pick you own funds” > “Featured Funds” > “Equity” > “Healthcare”, to learn more.Remarks:

While the healthcare sector faces various challenges such as labor shortages, regulatory pressures, and declining sales related to COVID-19 would continue to bring negative effect on certain stock names. However, the long-term outlook of the healthcare sector more than makes up for any near-term headwinds. The opportunity to generate returns that are not closely corrected – while simultaneously delivering benefits for patients – is becoming increasingly robust.Our Featured Funds Services consolidate investment ideas and hot funds1. “Healthcare” is one of the themes available in the Services. Log in to WeLab Bank app, tap the “GoWealth” at the right bottom corner > “Pick you own funds” > “Featured Funds” > “Equity” > “Healthcare”, to learn more.Remarks:(1) We categorise the funds into different investment themes set by us based on the funds' information and provide theme descriptions. Information relevant to the funds and categorisation is for reference only and does not constitute a solicitation, offer or investment advice.Importance Notice

This document is for general information only. The information or opinion herein is not to be construed as professional investment advice or any offer, solicitation, recommendation, comment or any guarantee to the purchase or sale of any investment products or services. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons.

The information or opinion presented has been developed internally and/or taken from sources (including but not limited to information providers and fund houses) believed to be reliable by WeLab Bank, but WeLab Bank makes no warranties or representation as to the accuracy, correctness, reliabilities or otherwise with respect to such information or opinion, and assume no responsibility for any omissions or errors in the content of this document. WeLab Bank does not take responsibility for nor does WeLab Bank endorse such information or opinion.

Past performance is not indicative of future results. WeLab Bank makes no representation or warranty regarding future performance. Any forecast contained herein as to likely future movements in interest rates, foreign exchange rates or market prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in interest rates, foreign exchange rates or market prices or actual future events or occurrences (as the case may be).

You should not make any investment decision purely based on this document. Before making any investment decisions, you should consider your own financial situation, investment objectives and experiences, risk acceptance and ability to understand the nature and risks of the relevant product(s). WeLab Bank accepts no liability for any direct, special, indirect, consequential, incidental damages or other loss or damages of any kind arising from any use of or reliance on the information or opinion herein. You should seek advice from independent financial adviser if needed.

WeLab Bank is an authorised institution under Part IV of the Banking Ordinance and a registered institution under the Securities and Futures Ordinance (CE Number: BOJ558) to conduct Type 1 (dealing in securities) and Type 4 (advising on securities) regulated activities.

This document is issued by WeLab Bank. The contents of this document have not been reviewed by the Securities and Futures Commission in Hong Kong.